No tax returns required

Bank Statement Loans for Self-Employed Borrowers

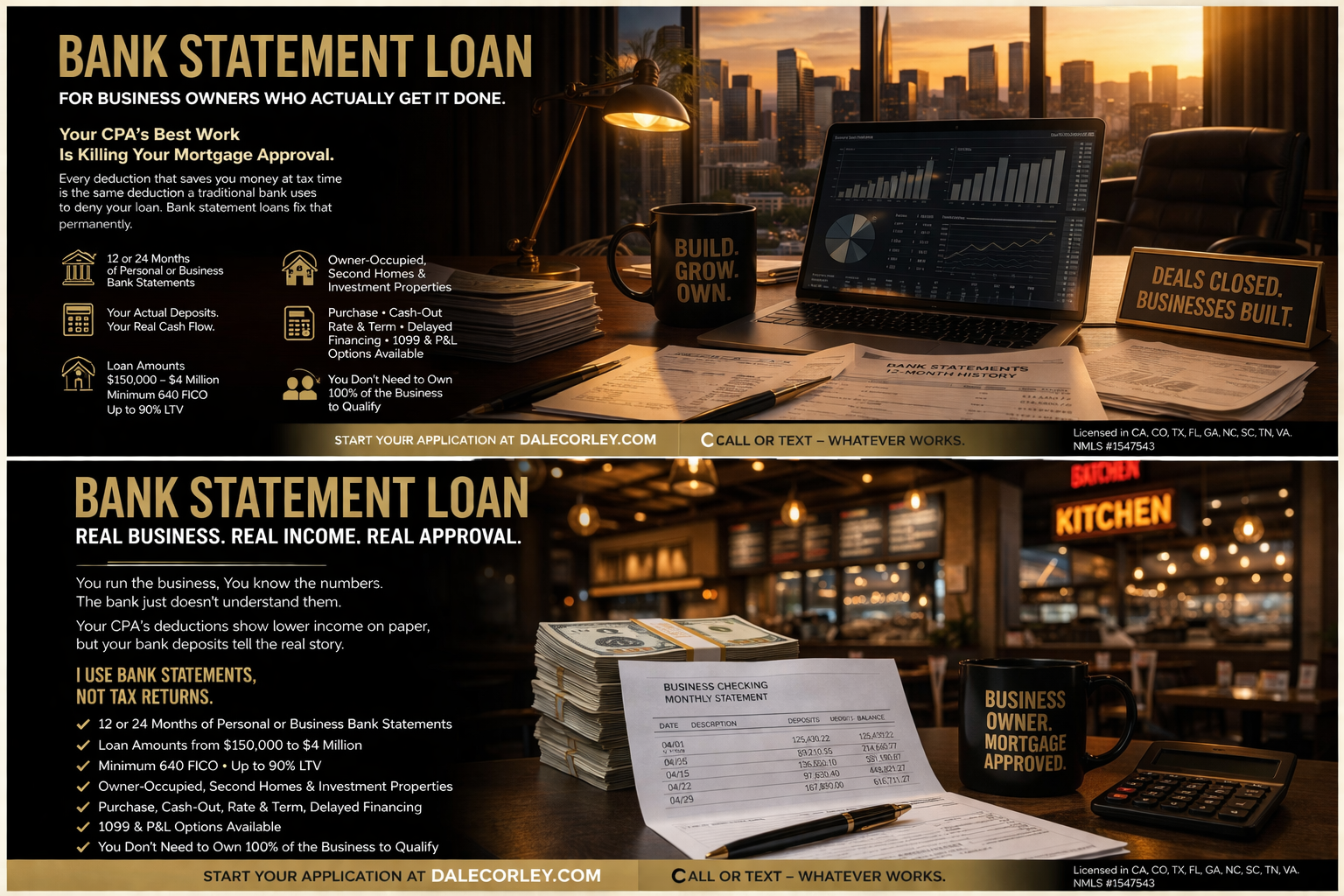

Qualify with 12–24 months of deposits — not tax returns. Built for business owners who write off aggressively.

Apply Now →OVERVIEW

What Is It?

A bank statement loan is designed for self-employed borrowers and business owners whose tax returns do not reflect their true cash flow. Instead of using taxable income, underwriting reviews 12 or 24 months of personal or business bank statements and calculates qualifying income from consistent deposits. This approach is common when deductions are legitimate but make W-2-style income look artificially low. Loan amounts and pricing depend on credit score, down payment, reserves, and how cleanly deposits are documented. I am licensed in multiple states and I specialize in helping borrowers understand what counts, what does not, and how to present a file that can actually clear underwriting.

QUALIFICATION

Who Qualifies

- Self-employed for at least 12–24 months (program dependent) with consistent business deposits

- Credit profile and down payment that meet investor requirements for bank statement programs

- Reserves after closing that meet guidelines for the loan size

- A clean narrative for large transfers, co-mingled accounts, or irregular deposit patterns

PROCESS

UNDERWRITING

How Income Is Calculated

- Step 1 — Collect statements. We gather 12 or 24 months of personal and/or business statements depending on the program.

- Step 2 — Expense factor. Underwriting applies an expense ratio to business deposits to estimate sustainable income.

- Step 3 — Qualifying monthly income. The net figure drives debt-to-income and supports the loan amount you can qualify for.

- Step 4 — Validate with supporting docs. We may support the file with a business license, CPA letter, or P&L depending on investor requirements.

NEXT STEPS

DOCUMENTS

What You’ll Need

- 12–24 months of consecutive bank statements (personal, business, or both, program dependent)

- Business license or evidence of self-employment

- Asset statements for reserves and down payment sourcing

- Purchase contract or refinance payoff information

- Identification and complete loan application

RISKS

What Can Go Sideways

- NSF items, gambling deposits, and unexplained large transfers can weaken a file — disclose early.

- Moving money between accounts without a trail can make deposits non-countable.

- If you are still running personal expenses through business accounts, expect extra questions.

CASE STUDY

Real Scenario

A restaurant owner showed strong daily deposits but low taxable income after legal write-offs. Traditional underwriting said no. We used 24 months of business statements, applied the correct expense factor, documented the business cleanly, and matched the file to an investor that understood the model. The borrower closed and kept operating the business the same way. This is the kind of loan banks will not touch — and The Mortgage Whiz closes.

FREE TOOLS

Embedded Calculator

Run a quick estimate, then talk to me for a personalized quote. Calculations are estimates only and do not constitute a loan offer.

This program pairs best with the calculator tool linked above. NMLS #1547543.

FAQ

Common Questions

Ready to Find Out Where You Stand?

No credit pull. No commitment. Just a straight answer on whether I can get you approved — and what it'll take.